In this post, I’ll quantitatively analyse VISA the US leader of payments.

Stock Price

Visa's stock has shown consistent growth, moving from the bottom left to the top right on the chart, with minor pullbacks that can be used as buying opportunities. Currently at its all-time high.

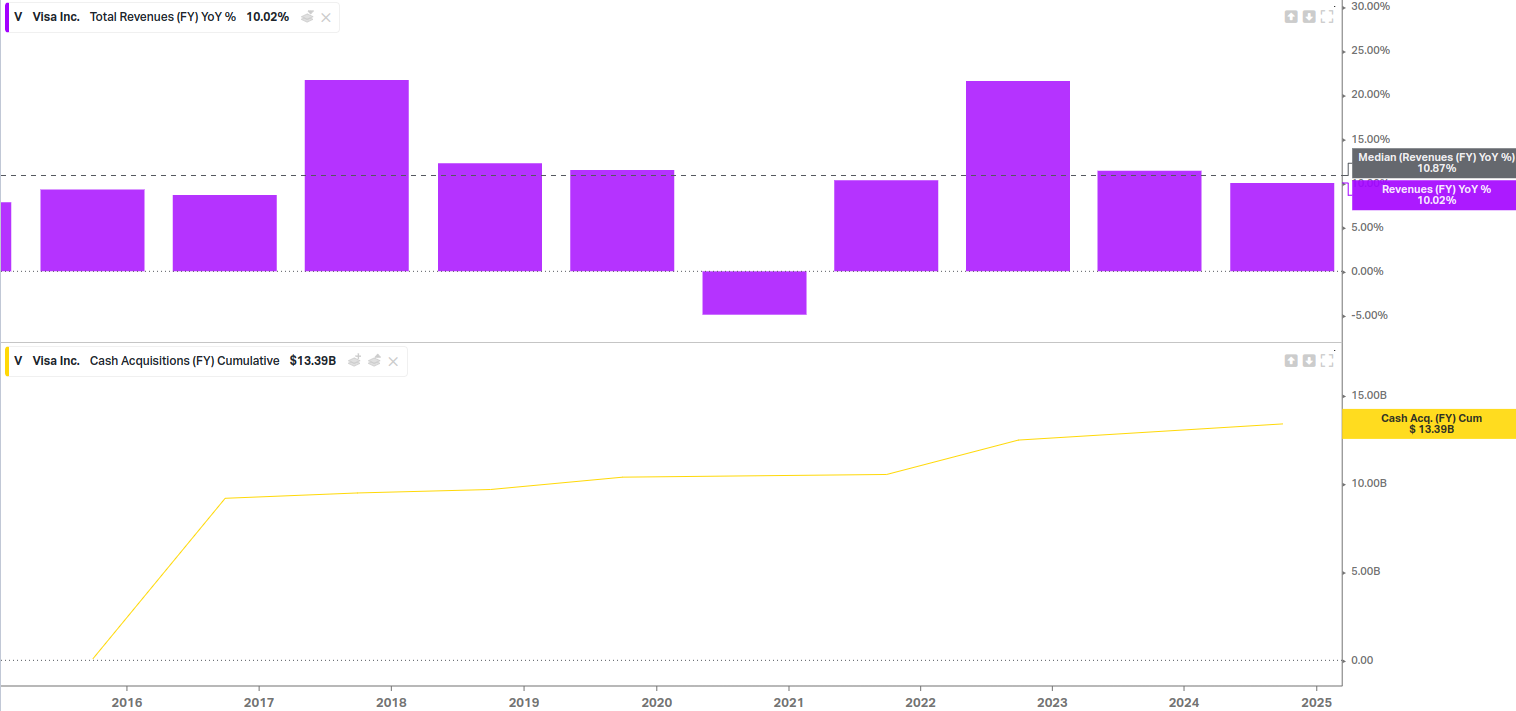

Revenues

Visa’s growth is pretty constant at around 10% throughout the decade.

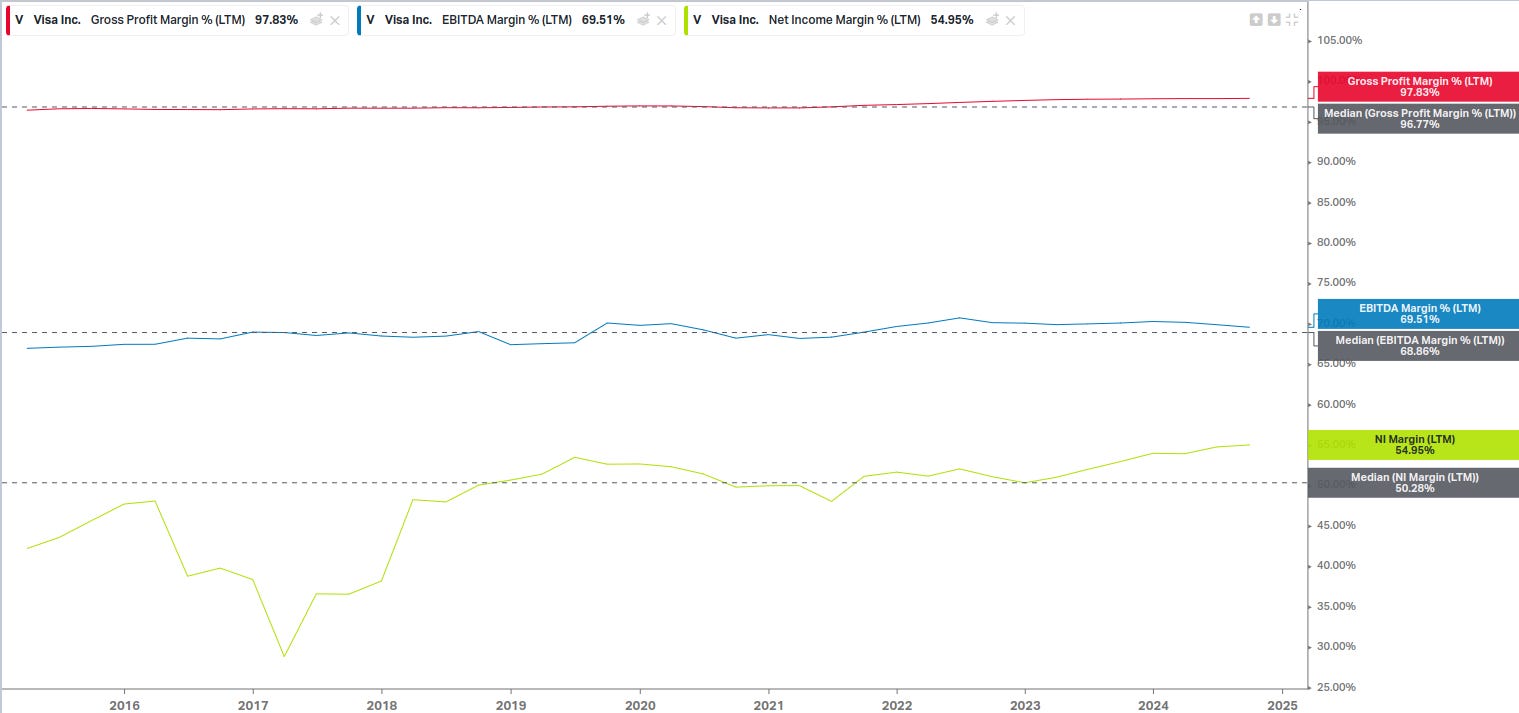

Profit Margins

Gross Margin: 98% - Reflecting Visa's monopolistic position in an oligopolistic market.

EBITDA Margin: 69% - Highly stable and indicative of superb operational efficiency.

Net profit Margin: Net margin has been increasing, reaching 55% over the period, showcasing Visa as a high-quality enterprise with margins that reflect this status.

Overall Margin Analysis: these margins are ones of the most qualitative of all listed stocks in the world.

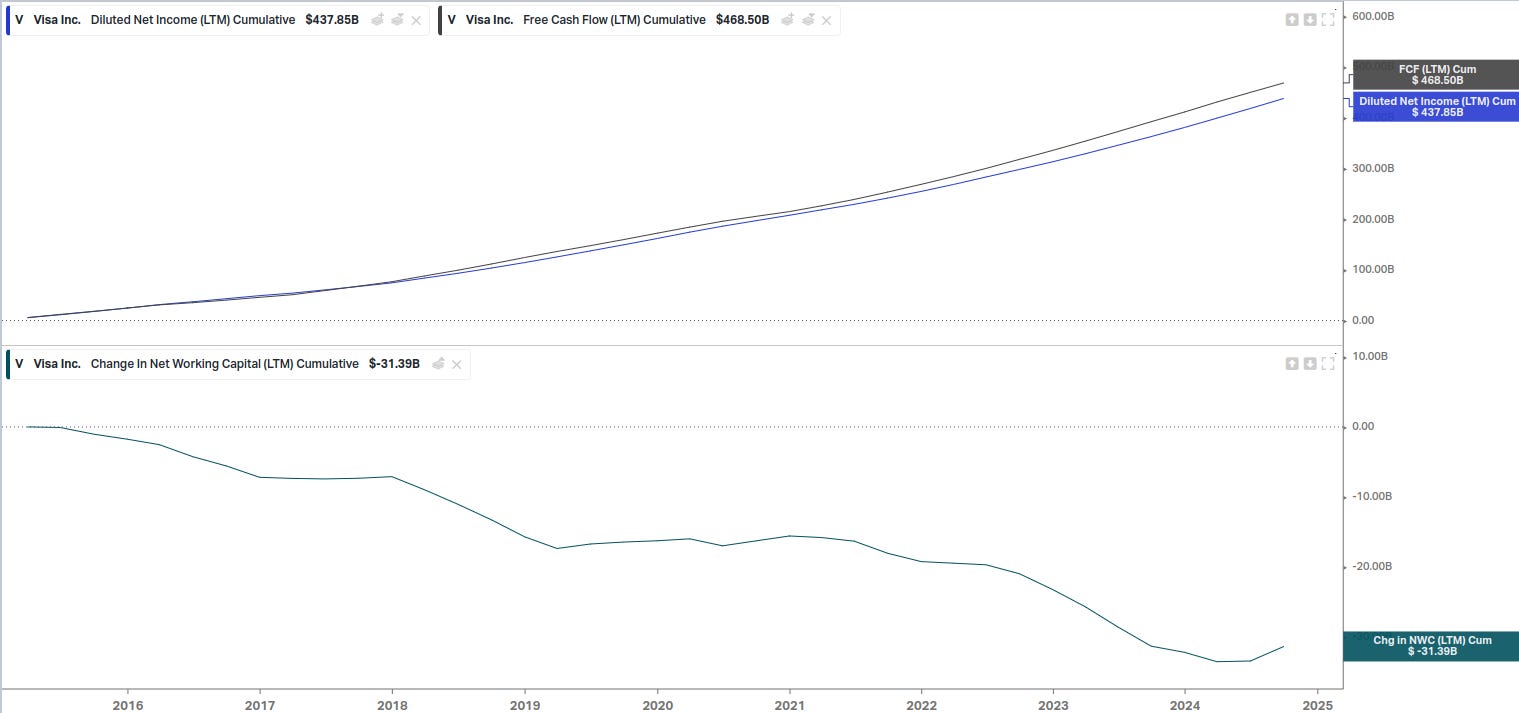

Quality of Net Profits

Conversion of profits into cash flow is excellent with free cash flow (FCF) exceeding net profits, largely due to improvements in working capital management.

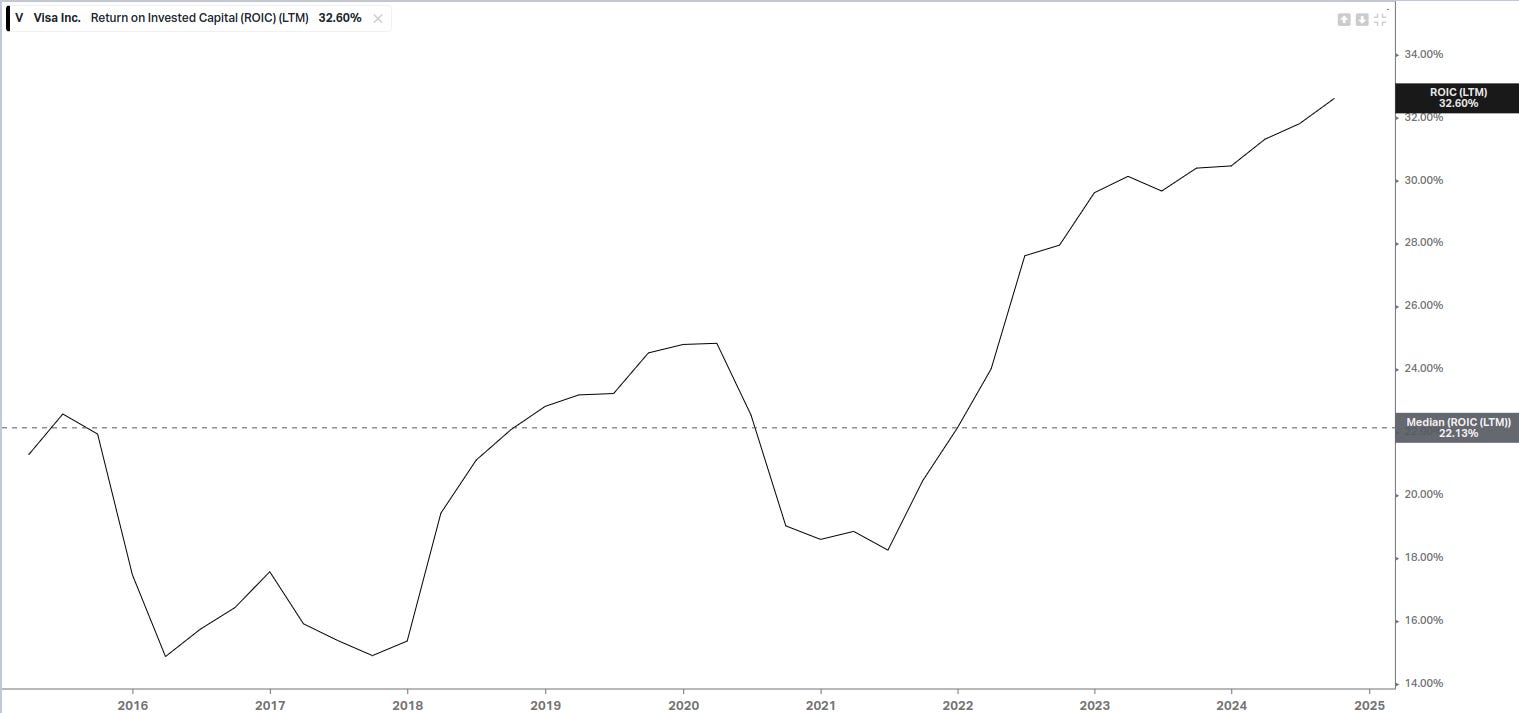

Profitability

Visa shows a business profitability of 32%, significantly higher than its growth rate, indicating the capacity for self-financing and shareholder returns.

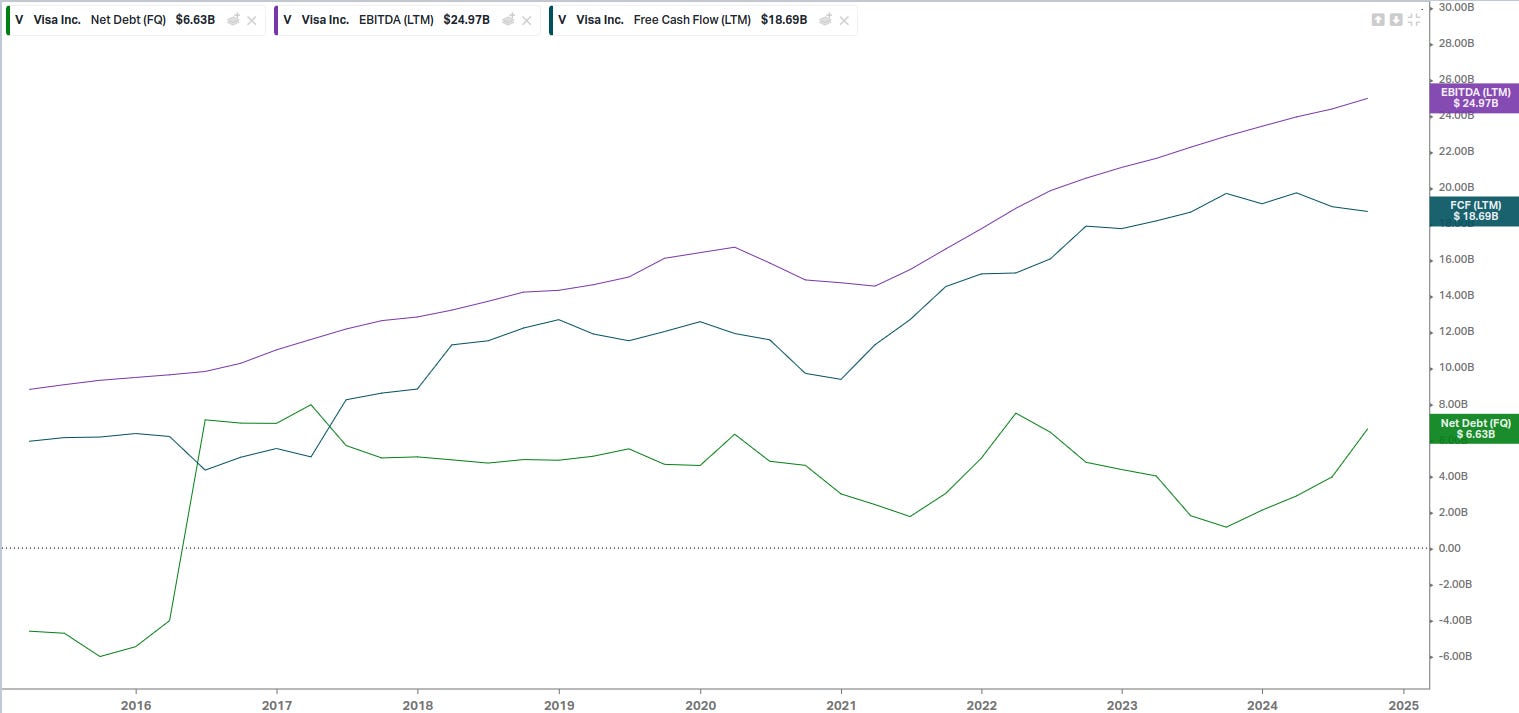

Debt

Net debt stands at $6 billion, which is 25% of EBITDA. This debt seems primarily used for acquisitions, given Visa's high profitability, there's no concern about repayment capability.

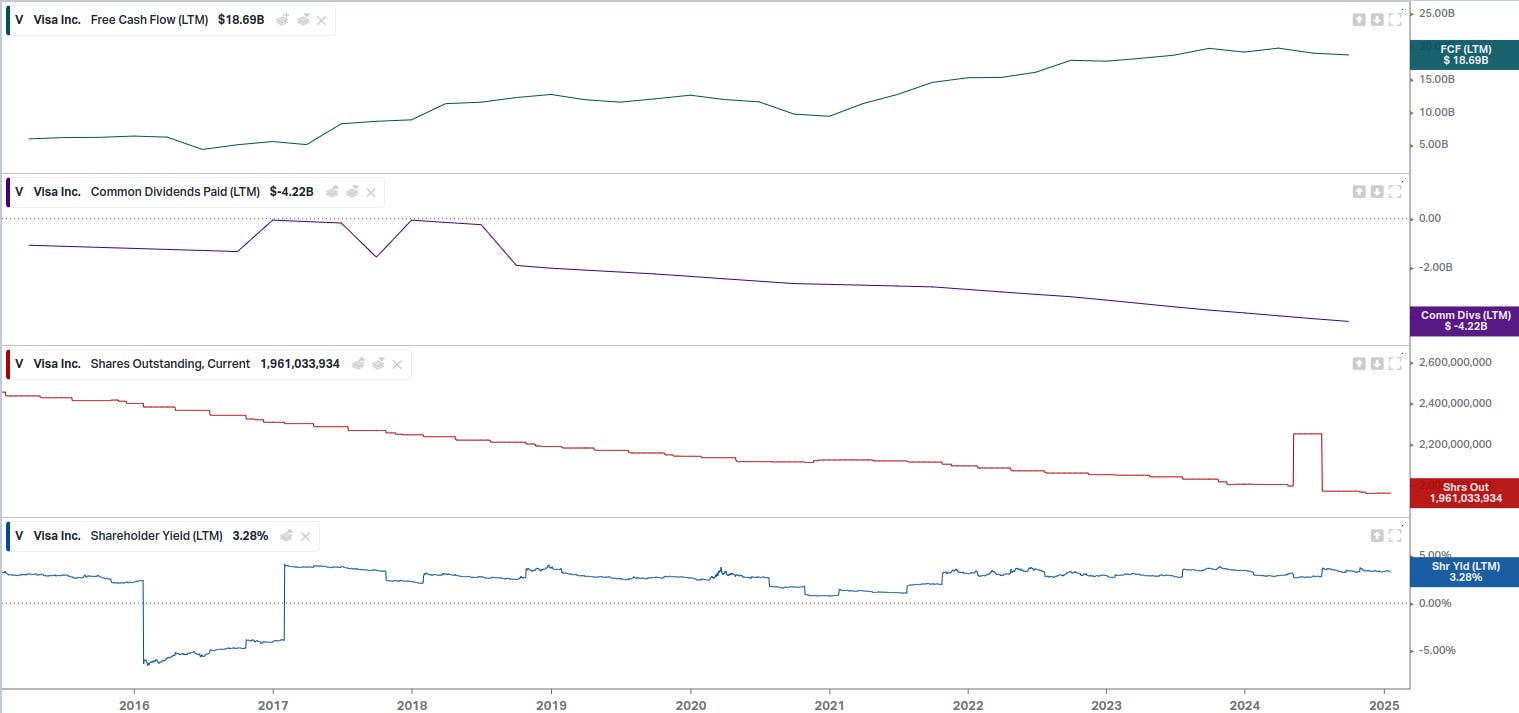

Shareholder Returns

Dividends: $4 billion in dividends out of $19 billion in free cash flow, the current yield is pretty low at less than 1%.

Stock Buybacks: Significant buyback program since 2008, reducing the share count and enhancing shareholder value.

Total Yield: The combination of dividends and buybacks provides a total yield of 3.3%, which is honorable but suggests a preference for buybacks over dividends for tax efficiency. That’s good because buybacks are more tax efficient than dividends.

Valuation

On an enterprise value to EBITDA basis, Visa typically trades at a median of 22.5 times. Currently, it's trading at a 15% premium over this, indicating no margin of safety at current valuation levels.

Conclusion

Visa represents an exemplary quality enterprise with sustained growth. For long-term investors (10-15 years), entering at the current price might still be beneficial due to the ongoing shareholder return strategies. However, there's no margin of safety for short-term investments (less than 3 years), as the price multiple might deflate, necessitating patience for price recovery.