In this post, I will quantitatively analyze ServiceNow, one of the leading American software companies.

Stock Price

The stock price of ServiceNow is at its highest since the start of its listing, with continuous growth.

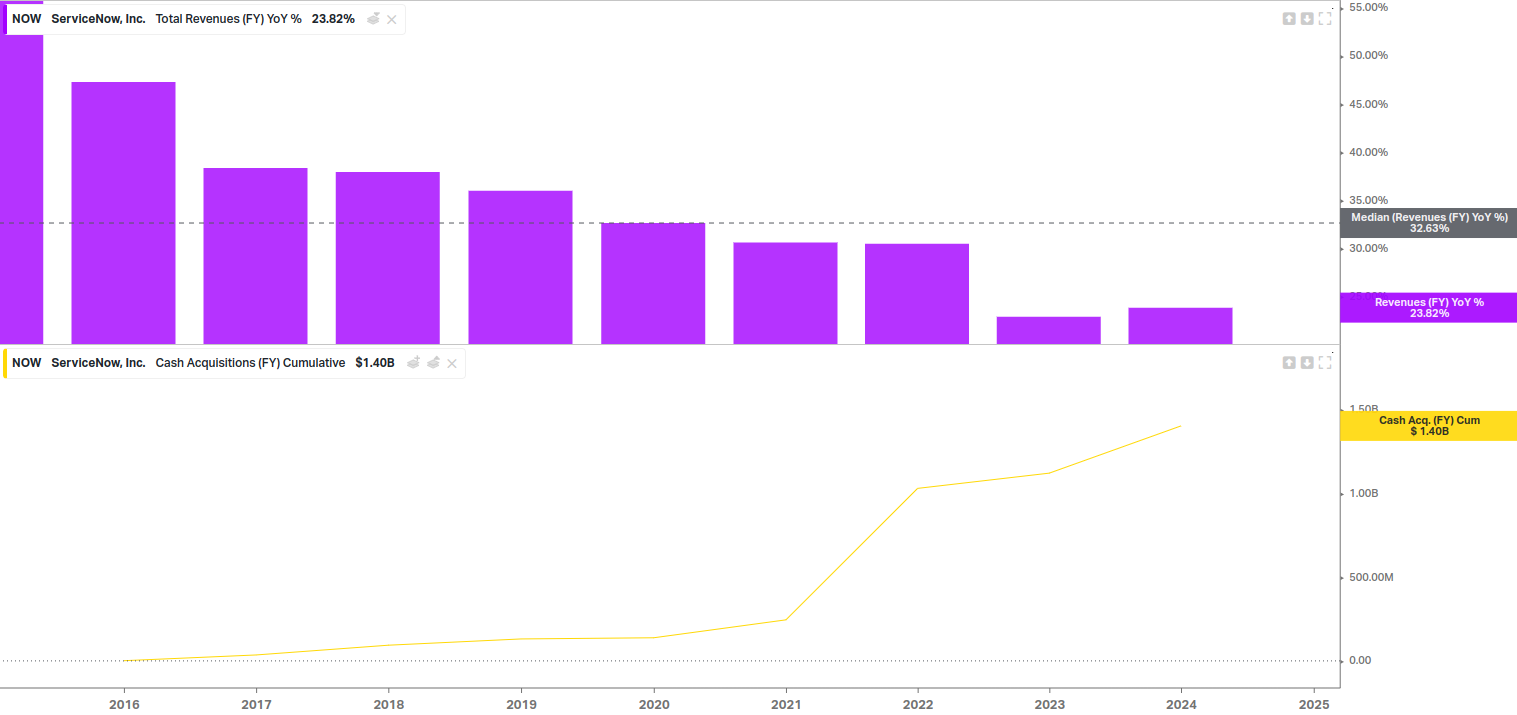

Revenue

Median growth of 38%, although this growth is slightly decelerating, it remains significant at 24% on the last publication.

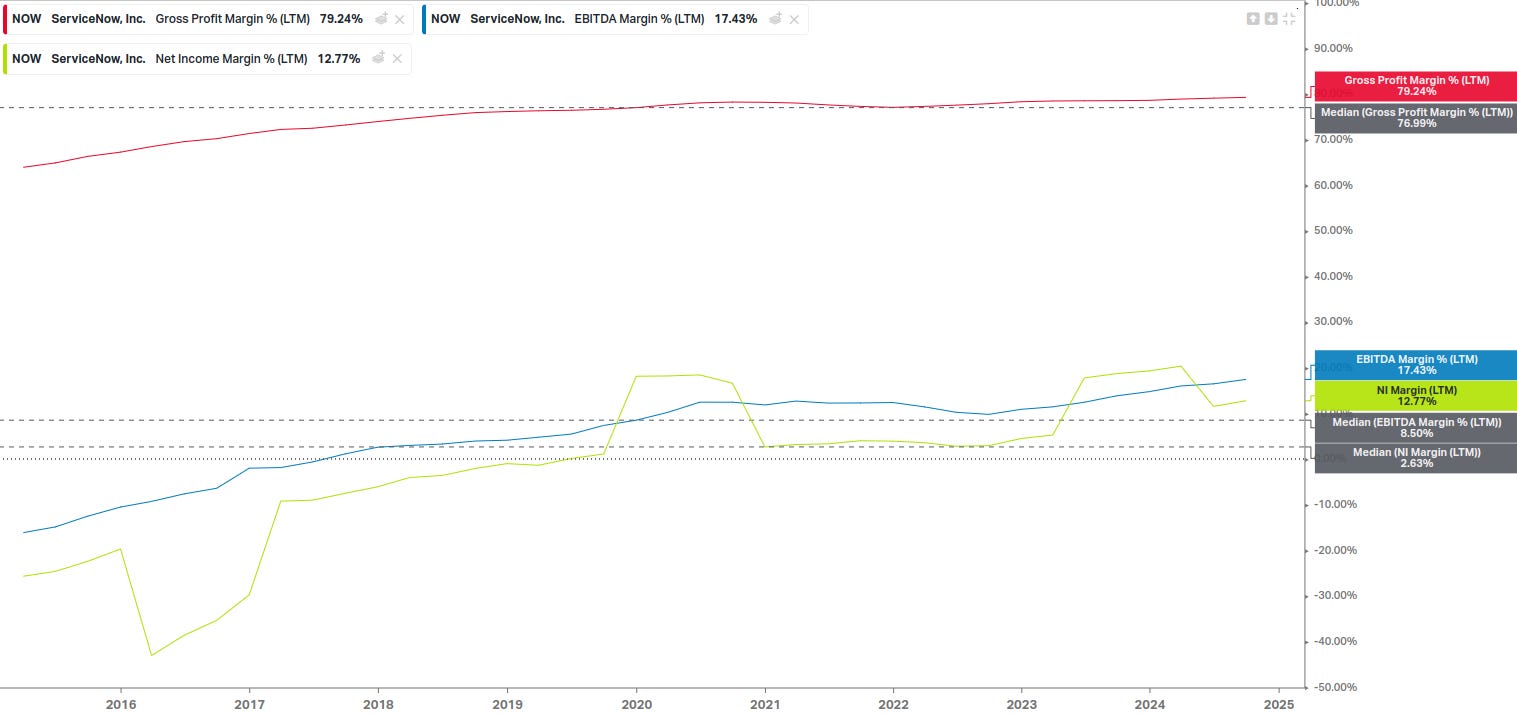

Profit Margins

Gross Margin: Increasing, at a near-monopolistic level, showing a significant competitive advantage.

EBITDA Margin: At 17.5%, increasing, indicating an improvement in operational efficiency.

Net Margin: At 13%, quite high for a company in a growth phase and profitable only since 2019.

Overall Margin Analysis: Margins show a positive trend with price increases and operational cost optimization, making the company increasingly profitable.

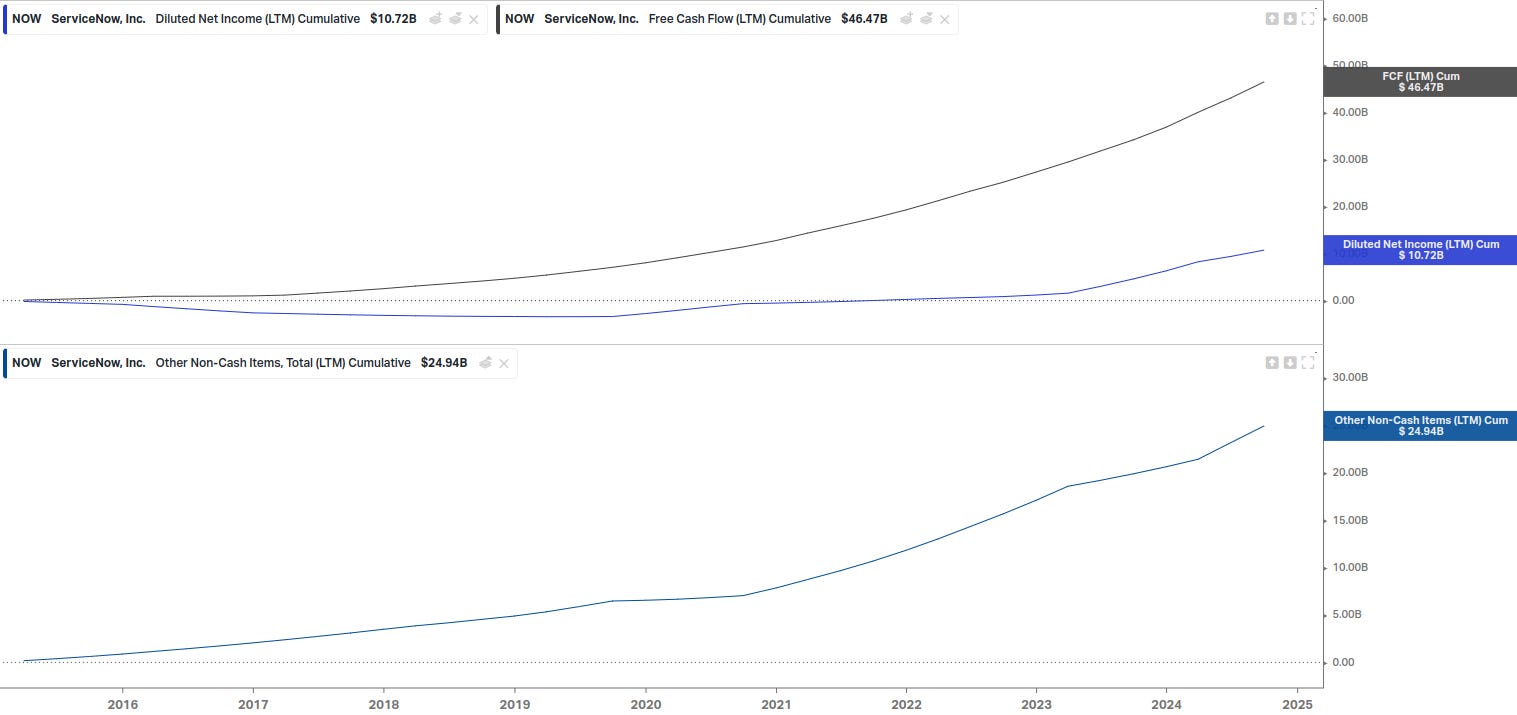

Quality of Net Profits

Net profits convert well into free cash flow, with free cash flow significantly higher than net profits, mainly due to non-cash items like stock-based compensation (16% of revenue).

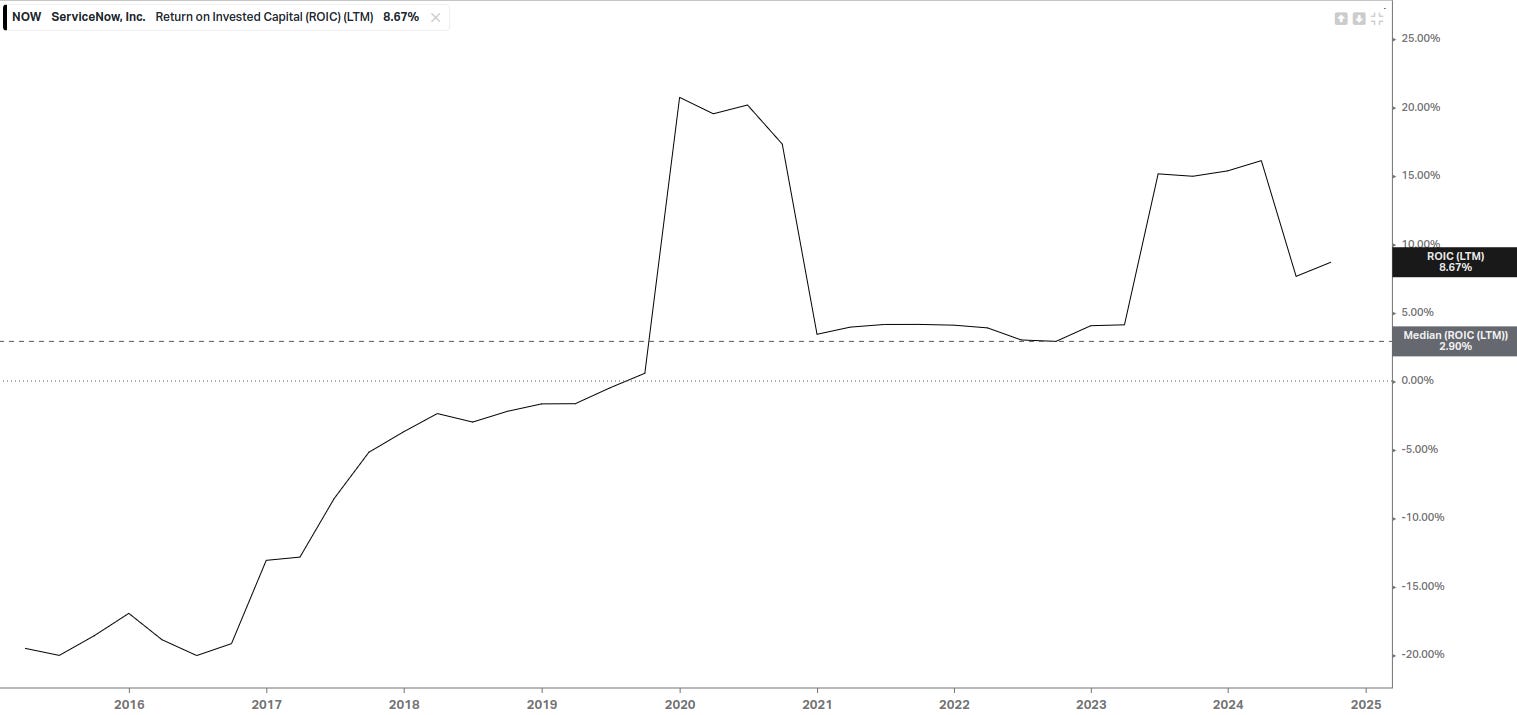

Profitability

Current profitability isn't huge (median at 8.5%, negative), but it's increasing since surpassing the break-even point in 2019, suggesting future improvement. With profitability slightly below growth, the company currently cannot self-finance its growth and must tap into its cash reserves.

Debt

The company has no debt and has an increasing net cash position, providing financial flexibility to fund growth or acquisitions.

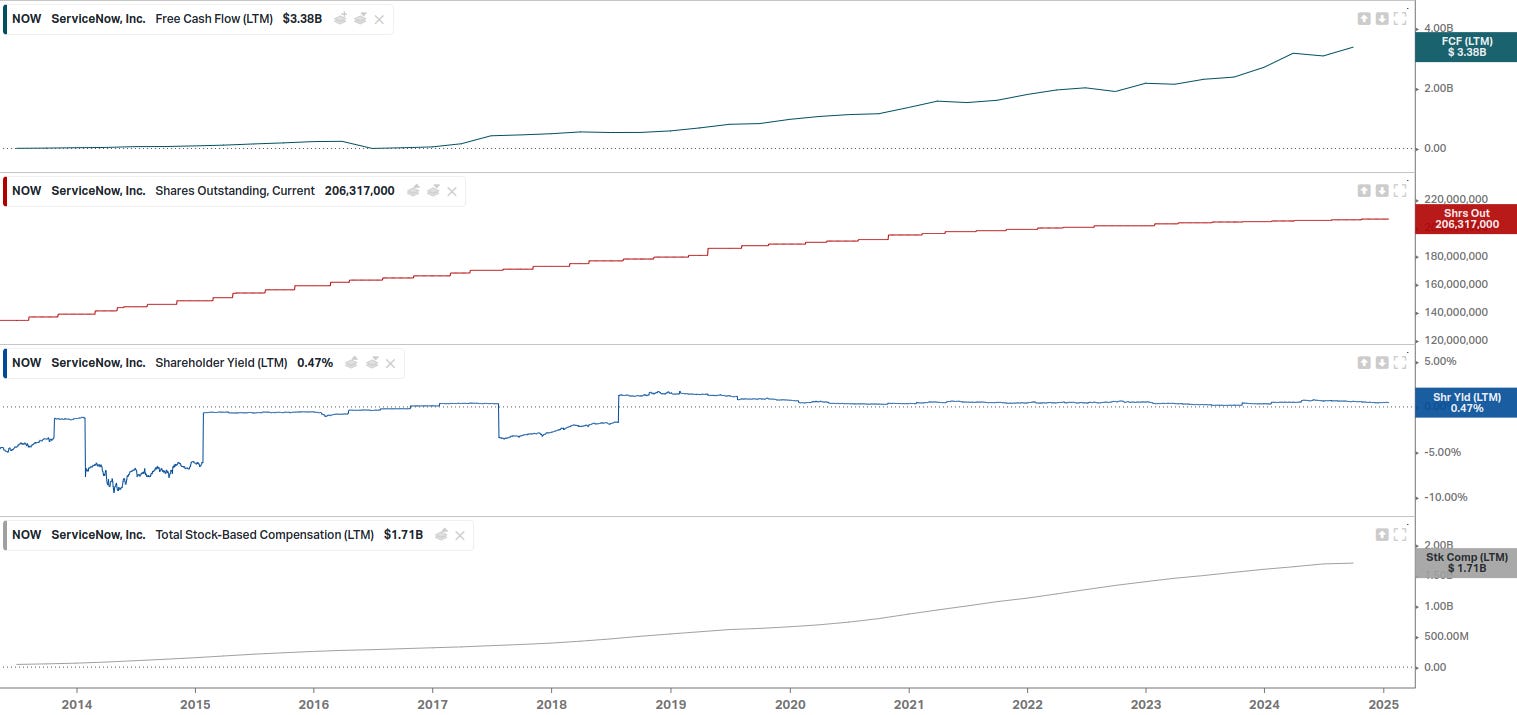

Shareholder Return

Dividends: No dividends are paid.

Share Buybacks: No share buyback plan to counteract dilution from stock-based compensation, leading to ongoing dilution of existing shareholders.

Total Return: Low due to the continuous dilution of shares.

Valuation

Price to Free Cash Flow: Median at 59, currently at 69, very high but justifiable for a growth company. The key with this type of case is to predict future cash flows, which is not easy.

Enterprise Value to EBITDA: At 115 for the last 12 months, extremely high, but this valuation is halved when considering the forecasted EBITDA for the next twelve months, although one must rely on analysts' predictions.

Conclusion

ServiceNow is a growth company with achieved net profits and increasing margins. Its current valuation might seem high, but it could be justified in a context of sustained growth and rising margins. However, for an investor focused on growth with a touch of quality, ServiceNow could be interesting in the long term, although there's a short-term risk of disappointment due to a weaker-than-expected report, which could lead to a contraction in multiples and a drop in stock price.